Norfund is committed to making a difference by ensuring that our capital contributes to outcomes that would otherwise not have happened. This is referred to as “additionality” and is a key criterion for Norfund’s investments.

The Norfund Act states that Norfund shall contribute to establishing viable, profitable undertakings that would not otherwise be initiated because of the high risk involved.

Proving the additionality of our investments is challenging because it requires insights into what could have happened had we not invested. Norfund substantiates additionality claims by evaluating all potential investments against our additionality framework. We also have portfolio level KPIs and thresholds that ensure that we allocate capital to instruments and markets with high inherent risk.

What does it mean that an investment is additional?

Financially additionality

An investment is financially additional when the private sector partners are unable to obtain financing from capital markets (local or international) for a specific activity at the necessary terms and/or scale, or where it mobilises finance from the private sector that would otherwise not have been invested.

Value additionality

An investment is value additional in cases where the investor adds non-financial value, alongside its investment, to private sector partners that the capital markets would not offer, and which will lead to better development outcomes. It is often pursued through active ownerships (e.g. board participation), capacity building activities, advisory services and other technical assistance and other ways.

Development additionality

Development additionality is that the investment will deliver development impact that would not have occurred without the partnership between the official and the private sector.

Ten ambitions on additionality

Norfund has a defined additionality framework that helps assess the additionality of our investments and ensure alignment with the OECD definition. This framework consists of ten additionality ambitions (see table below) reflecting both the financial and value additionality of our investments. For each ambition, we have identified relevant indicators to assess the extent to which we meet these ambitions. Investments under the Climate Investment Mandate are subject to the same additionality assessment. Development additionality is assessed for each new investment by setting baseline and target values for key impact/ climate ambitions, describing what the investment aims to achieve.

Norfund’s additionality in an investment depends on many factors and the additionality framework tries to capture different aspects of additionality. Investments are scored 1-10 based on how many additionality ambitions they trigger.

We have revised the framework twice since 2018, based on our user experience and to better reflect the markets we operate in. From 2025, we will implement a revised additionality framework to comply with updated OECD-DAC Private Sector Instrument requirements for additionality.

More information on which ambitions each investment is particularly additional on, is listed on the individual pages of each investment in the investment overview on Norfund’s webpage.

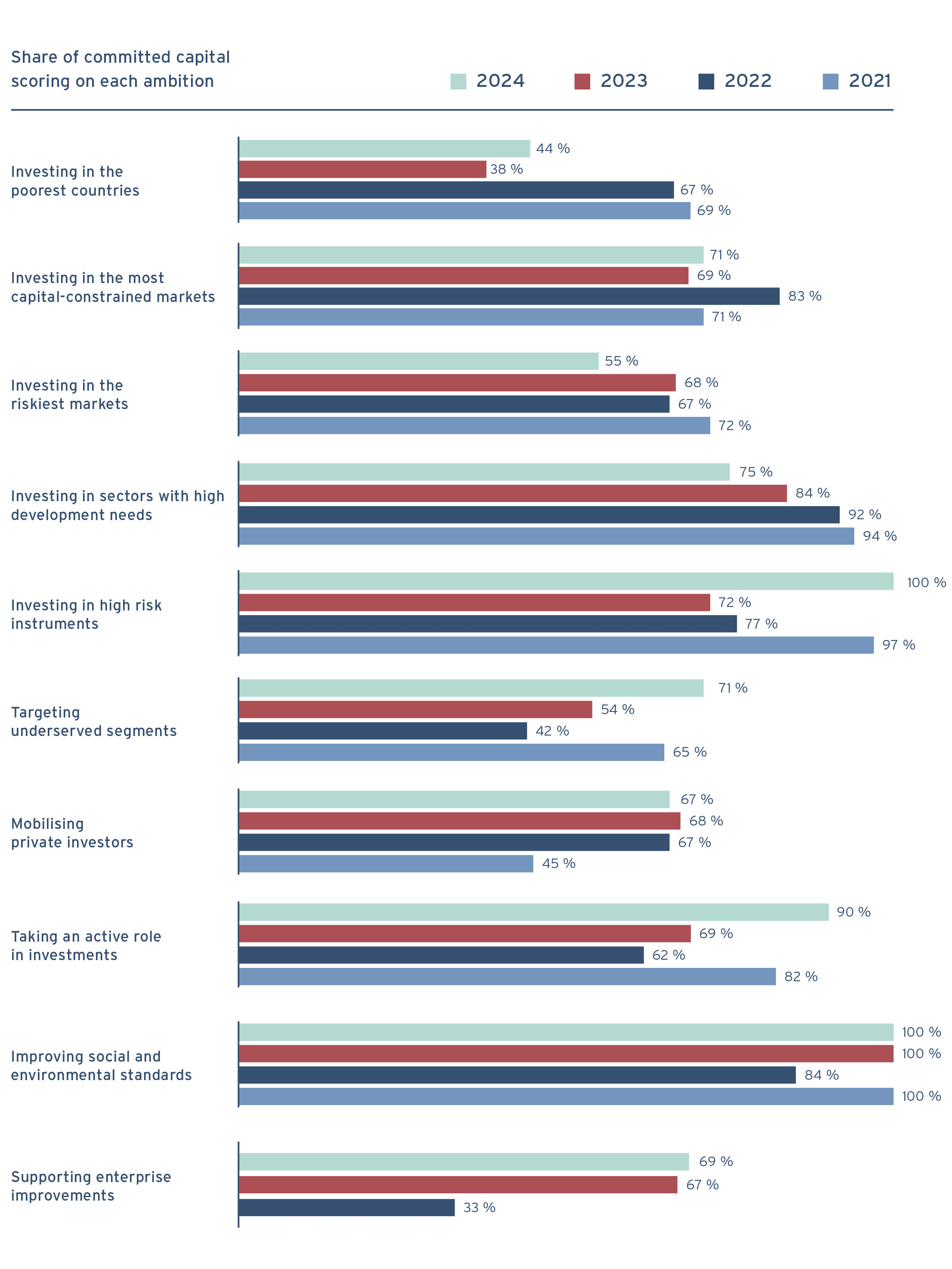

Percentage of committed capital to new projects in 2024 scoring materially on each additionality ambition (follow-on investments are not included):

Since 2022, the overall share of investments scoring on the additionality ambition “Investing in the poorest countries” has declined. This is partly due to the introduction of the Climate Investment Fund as well as expected annual fluctuations. Generally, projects in the poorest countries have smaller ticket sizes, which means they take up a relatively smaller share of total committed capital. 11 out of 27 new projects in 2024 scored on this ambition, which illustrates the high level of activity towards these countries in Norfund.

More than two thirds of the committed capital in 2024 targeted sector-specific underserved segments, meaning the beneficiaries are underserved business types or end-clients. This could for instance be a loan issued to a financial institution targeting microenterprises or an investment in a company providing off-grid solutions to poor households.

All the capital Norfund committed in 2024 were with high risk instruments. This includes equity, various quasi-equity instruments, local currency loans, and debt with long tenor. Norfund’s willingness to take on more risk than what the market normally is willing to accept is central to our additionality, and as such this is a positive development.