Strategy for the Climate Mandate

2022-2026

The Climate Investment Fund is Norway’s most important tool in accelerating the global energy transition by investing in renewable energy in developing countries with large emissions from coal and other fossil power production.

To help developing countries build their economy on the backbone of renewable energy, the Climate Investment Fund will allocate 10 billion NOK from 2022-2027 to invest in renewable energy and low carbon technologies.

Aim

The Climate Investment Fund shall contribute to reduce or avoid GHG emissions from coal fired power and other fossil energy production and ensure that economic growth is built on low carbon technologies through investments in renewable energy and enabling technologies in emerging markets where GHG emissions are or are expected to become large.

Climate mandate

Within our mandate, we need to prioritize. Our strategic choices with respect to prioritization have been assessed against three criteria: climate impact, additionality and feasibility. Our strategy builds on strategic choices along nine dimensions that will allow us to effectively invest the funds in line with the given mandate.

Management

Norfund will manage the fund on behalf of the Ministry of Foreign Affairs. The investments under the Climate Investment Fund will be made under Norfund’s own name, but the fund’s investments and portfolio will be managed separately from Norfund’s other activities.

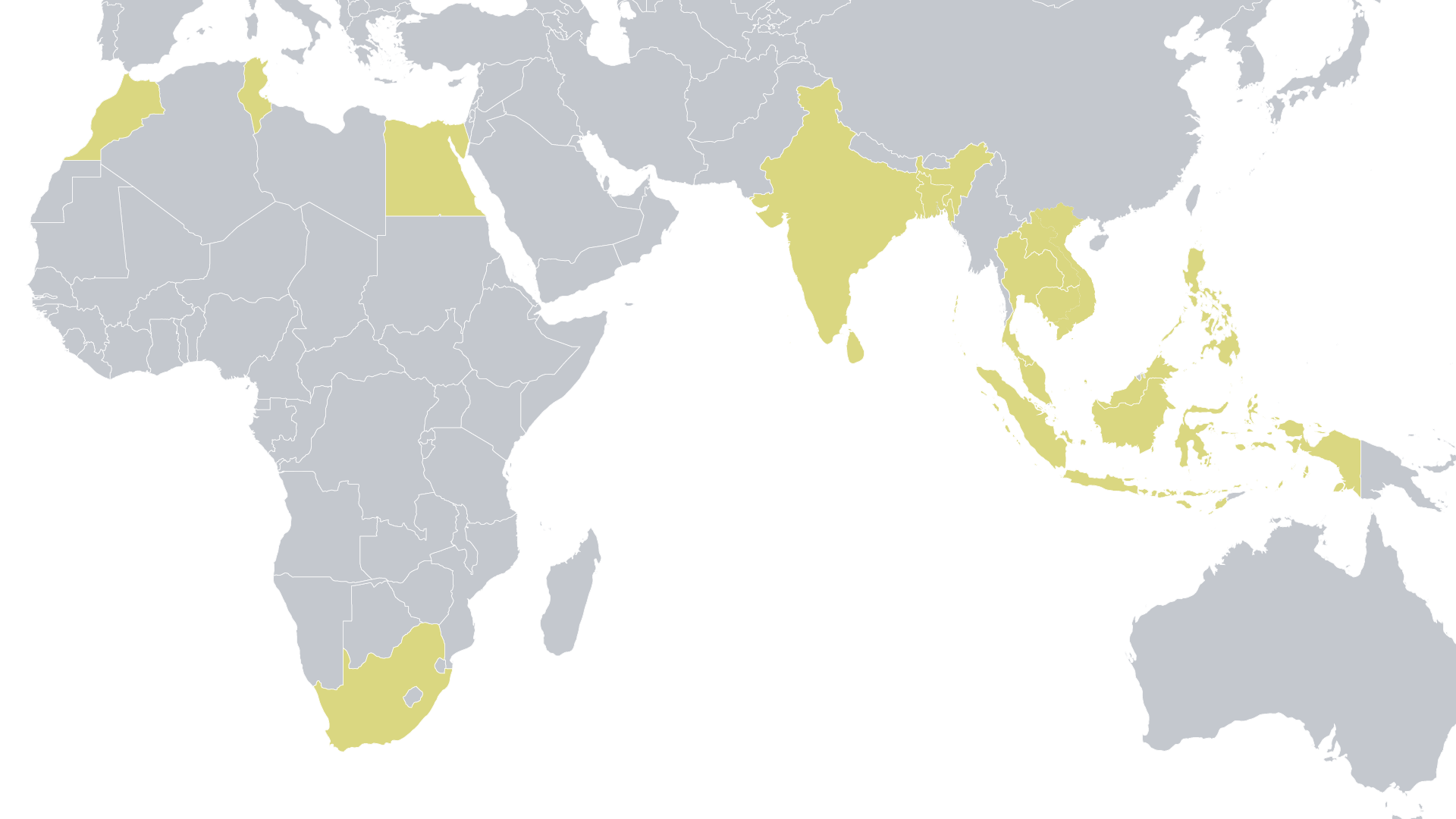

Geography

Through the climate mandate, Norfund prioritizes 13 core countries in North and Southern Africa, and in South and Southeast Asia. We will allow exposure limits of up to 25% for large, core countries such as India and South Africa.

Sectors

We will invest in both large scale renewables such as wind farms and smaller C&I opportunities such as rooftop solar. We may also invest in enabling technologies with high climate impact (e.g., storage, transmission), focusing on verticals where Norfund has strong competences, can be additional and where there are investable opportunities in our markets.

Ambitions

The climate fund have the following ambitions to measure how successful we have been in delivering on the mandate:

- 9 GW new renewable energy capacity financed

- 14 million tons CO2 avoided per year – equivalent to 30% of Norway’s annual GHG emissions

- 1 billion NOK invested into “next wave” technologies

- 10x multiplier effect per dollar invested by Norfund

Risk profile

The CIM will adopt the risk appetite statement of Norfund, but with the opportunity to take somewhat higher technology commercialization risk. In this way, Norfund can help accelerate the implementation of clean energy technologies in our markets through investments that private sector players hesitate to take on.

Partners and platforms

The climate mandate will, in line with Norfund’s overarching strategy, aim to establish new as well as strengthen existing platforms and partnerships. This strategy of sharing risk can enable industrial investors to realize more projects or enter into new markets, thereby multiplying the impact of Norfund’s capital, and leading to sustainable business ventures.

Exits

Under the CIM we have an ambition to actively seek exit of mature or de-risked investments to circulate capital and multiply the climate impact we can have per dollar committed to the fund. To achieve this, we will build on the improving practices regarding exits already emerging for the past years, including assessing exit opportunities at investment and structure investments with exit in mind.