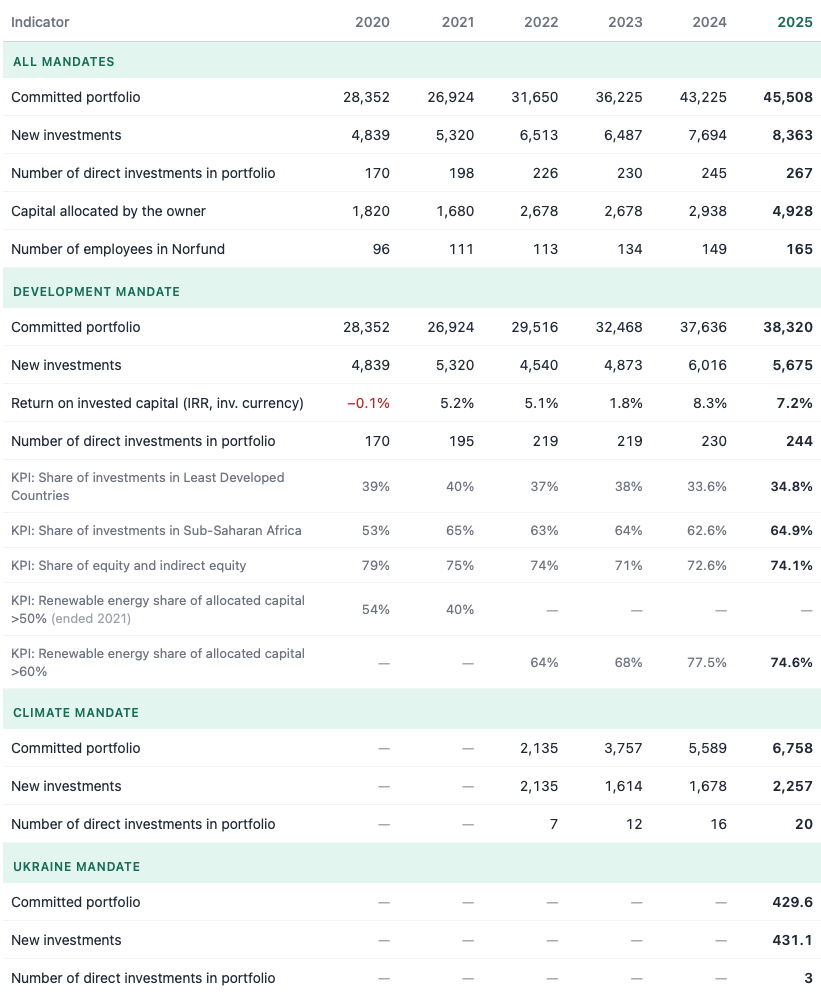

Key figures

While the full impact of Norfund’s investments is impossible to quantify, we work to measure the development effects our portfolio companies generate. Below you’ll find a collection of our most important figures.

For a complete overview of Norfund’s 2025 figures, see our annual report ->

Commitments

8.4 billion

new commitments (NOK)

45.5 billion

total portfolio (NOK)

More about our financial results->

Mobilisation and costs

17.8 billion

mobilised private capital (NOK)

attributed according to OECD Methodology (preliminary estimation)

1.16 %

operating cost

of committed portfolio

Investments

34

new investments

in 2025

24

follow-ons

in 2025

267

direct investees

in our portfolio

1,114

indirect investees

in our portfolio

Jobs

788,000

total jobs

in portfolio companies

29,000

jobs created in 2025, net

in portfolio companies

40 %

female employees

in portfolio companies

More about job creation in Norfund’s portfolio companies ->

Energy access and supply

1.65 million

new households

granted access to electricity in 2025

25.4 TWh

electricity produced

by portfolio companies in 2025

12,3 GW

new capacity

total new renewable capacity financed in 2025

More about energy access and supply ->

Access to finance

12.7 million

new clients

offered financial services in 2025

158million

total clients

offered financial services in 2025

87.3 billion

increase in lending volume

(NOK)

More about access to finance ->

Avoided emissions

10.3 million

tCO₂e actual avoided emissions

by greenfield assets in 2025

22.7 million

expected tCO₂e

avoided emissions annually from 2025 investments (Climate Investment Fund)

Read more about avoided emissions ->

Taxes

41 billion

taxes paid in 2025 (NOK)

4.2 billion

increase in taxes paid by portfolio companies (NOK)

Read more about tax revenues ->

IRR

Internal rate of return

7.8 %

in 2025, across mandates

in investment currency

5.3 %

since inception, across mandates

in investment currency

13.3 %

since inception, Climate Investment Fund

in investment currency

5.2 %

since inception, Development Mandate

in investment currency

Read more about our financial returns in 2025 ->

Read more about our financial results in general ->

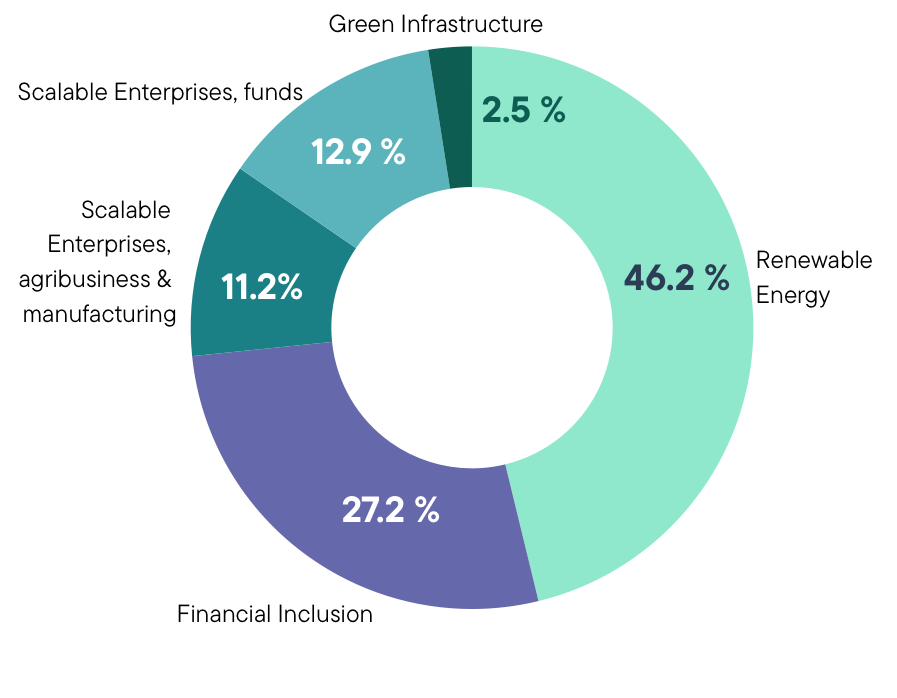

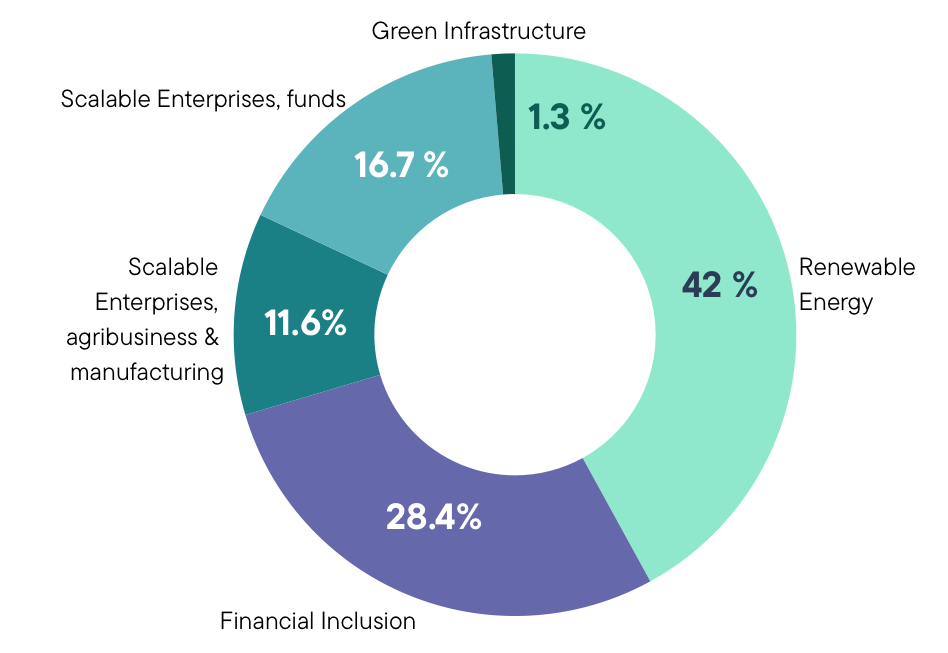

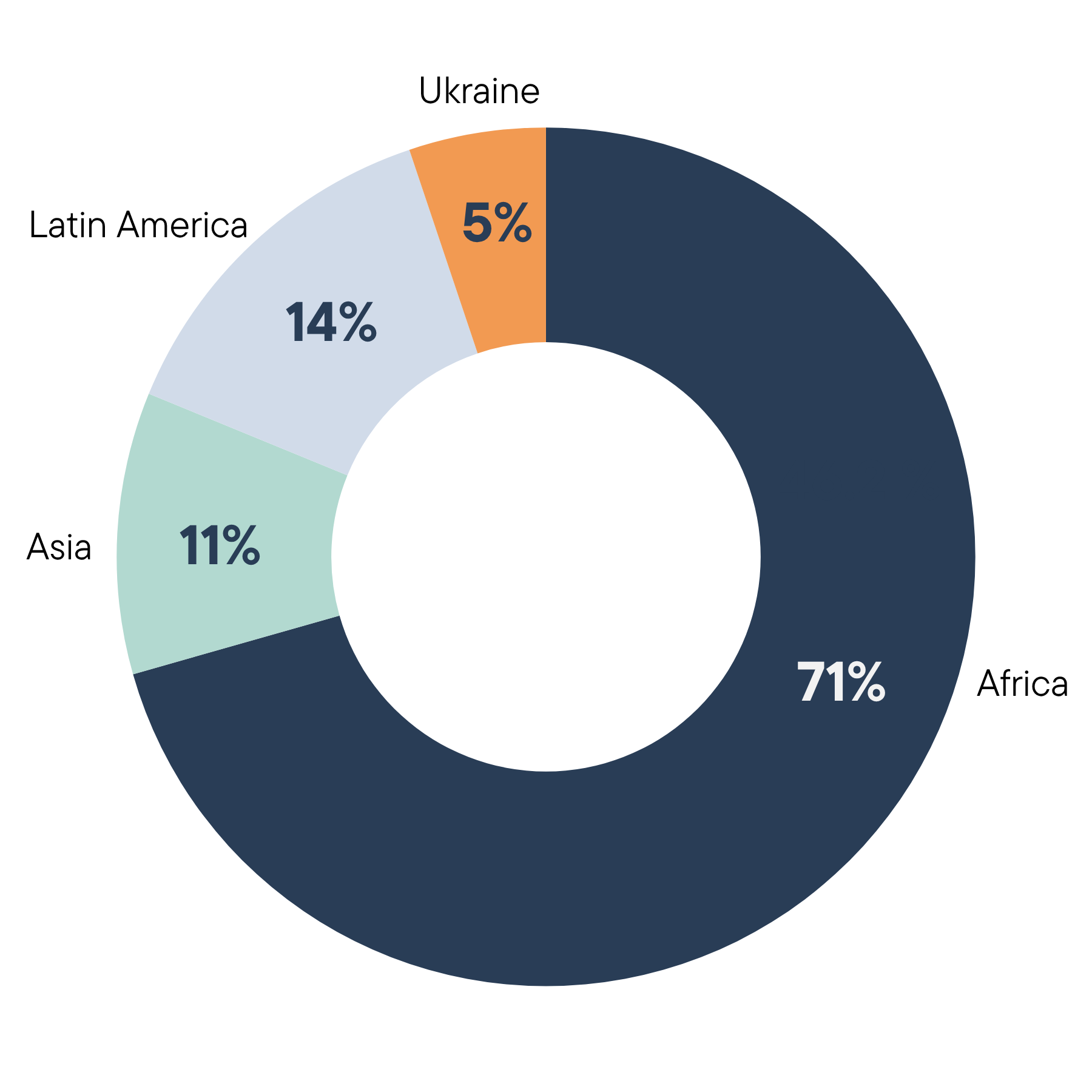

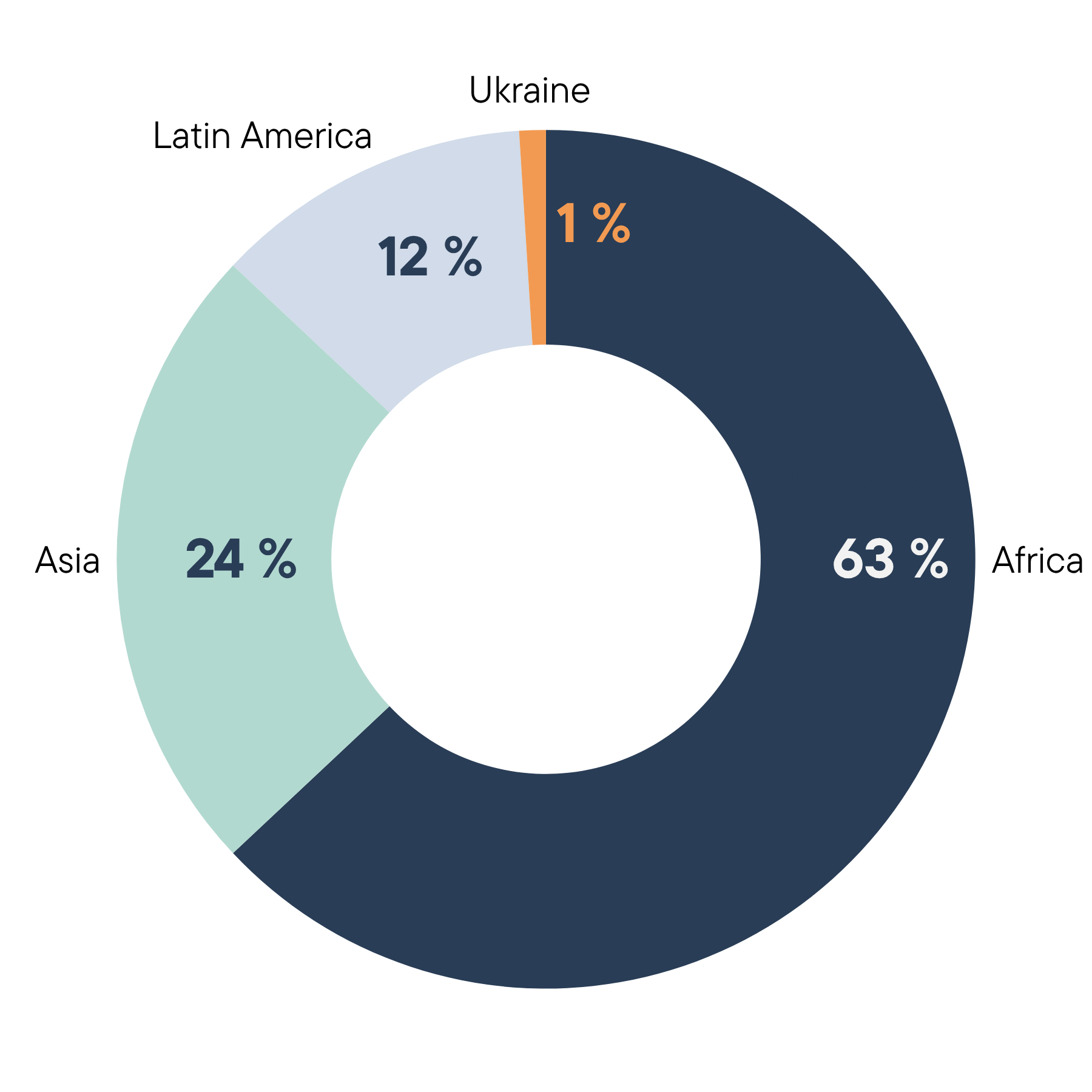

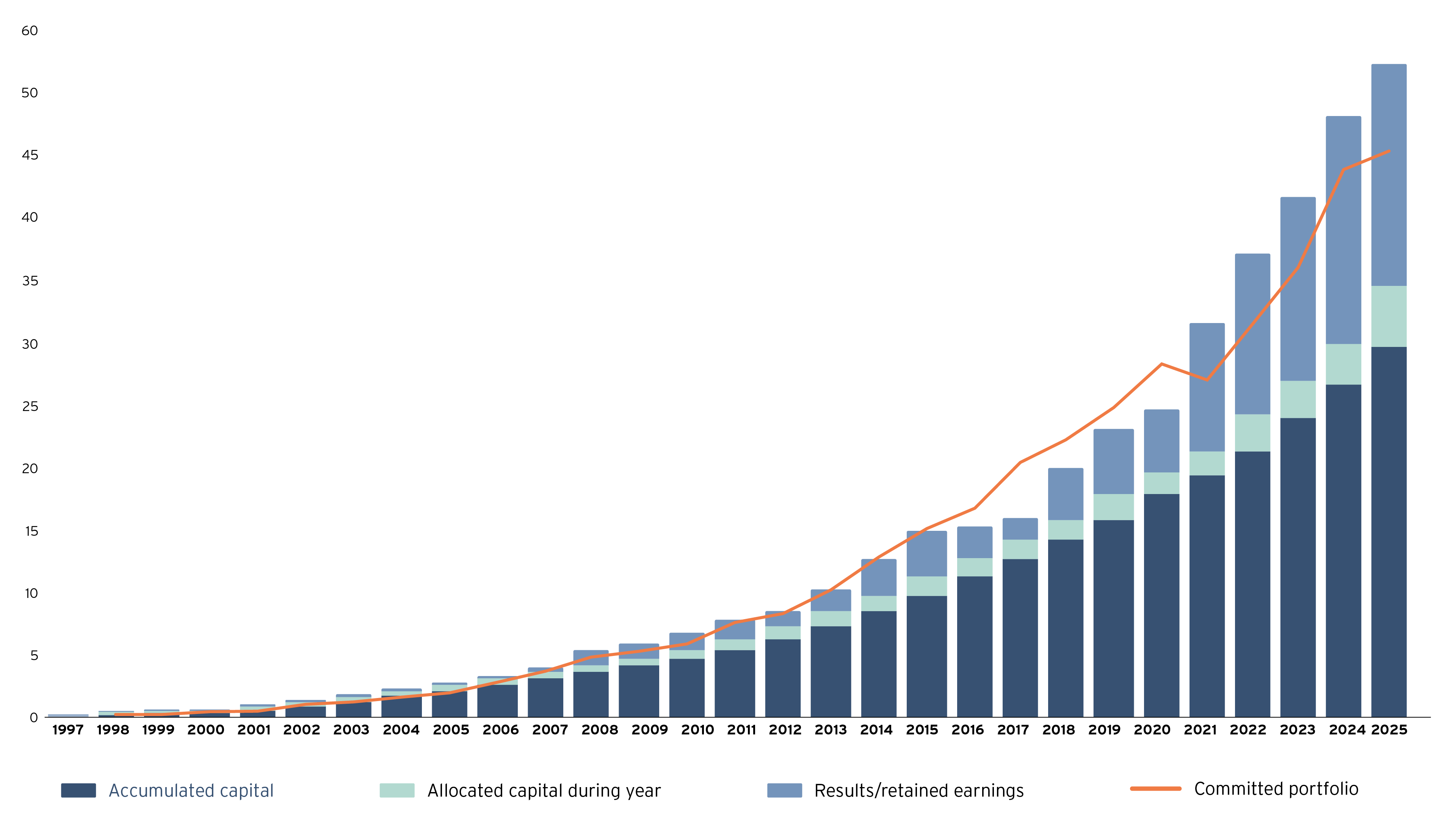

Portfolio breakdown in 2025

New commitments per investment area

Portfolio per investment area

New commitments per region

Portfolio per region

Portfolio since inception, billion NOK

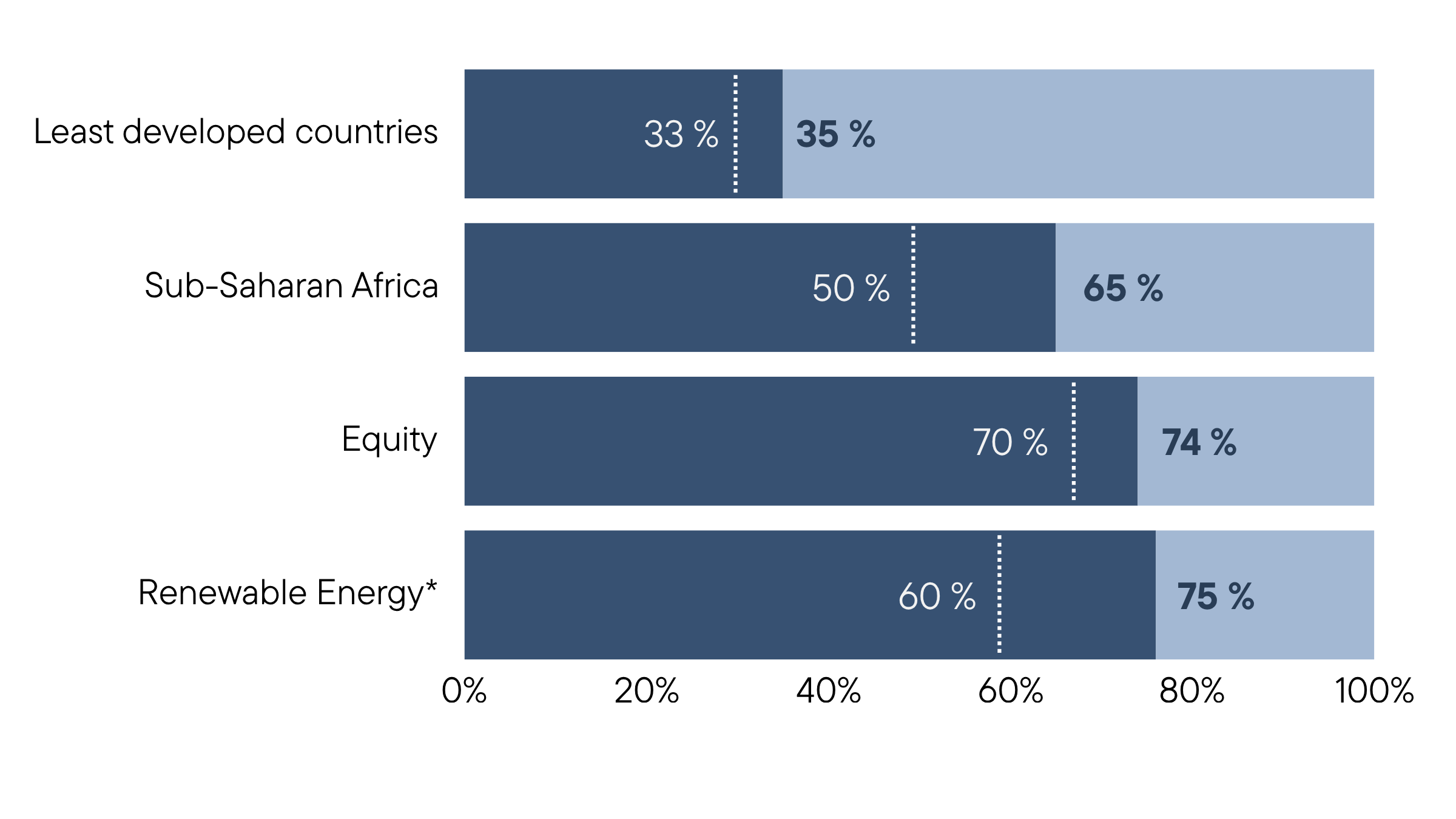

Key Performance Indicators

Development mandate

Four key performance indicators (KPIs) have been developed for the Development mandate (see table below):

*The RE KPI was new for 2022 and is different from the other portfolio KPI’s. The RE KPI is defined as total RE-commitments (at commitment date fx-rate) divided by total allocation from MFA, starting from 2022. This should over time be at least 60%.

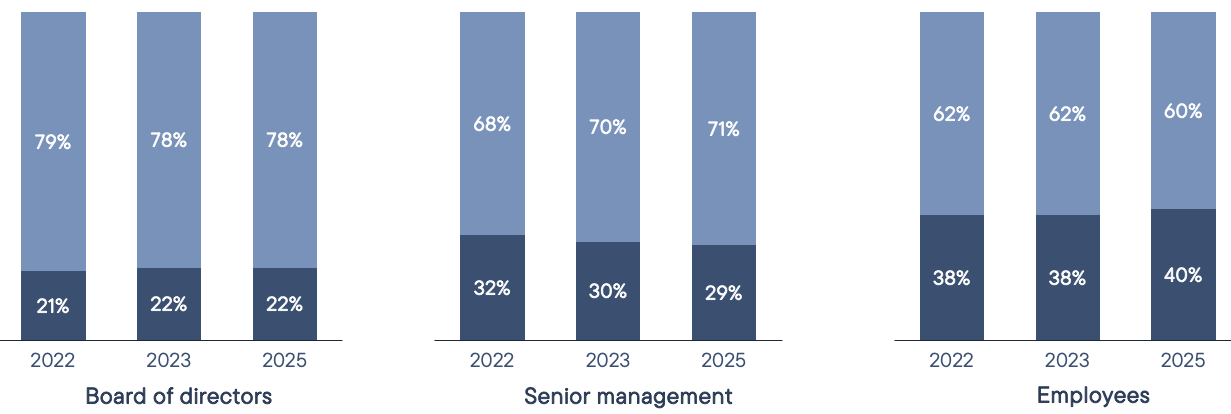

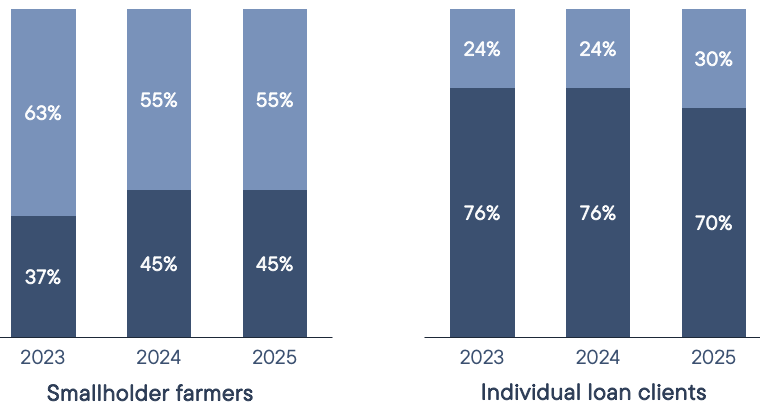

Gender balance in Norfund’s portfolio companies

Status 2023-2025

Read more about our work with gender equality ->

Key figures per year